For Further Information Contact:

Switzerland Update: Partial Revision of the VAT Act: Introduction of Platform Taxation as of 1 January 2025

11/11/2024From 1 January 2025, significant changes to VAT law will come into force in Switzerland. The Federal Council has implemented the partial revision of the Value Added Tax Act (MWSTG) and the revised Value Added Tax Ordinance (MWSTV) adopted by Parliament.

The focus of the partial revision is on the introduction of platform taxation. This blog post explains what is meant by this and how the changes will affect the affected parties.

Background of platform form taxation

Since the last VAT revision, which came into force in 2019, mail order companies that deliver goods to Switzerland are subject to VAT if they generate a turnover of at least CHF 100,000 with small consignments (import tax amount below CHF 5). However, it has been shown that the effect of this measure is limited, as many smaller mail-order companies do not reach the required turnover limit. From 1 January 2025, companies that enable the sale of goods via an electronic platform are therefore to be included in the collection of VAT. From now on, operators of electronic platforms will be regarded as service providers for all sales they broker. This applies to both domestic and foreign platform operators.

Affected electronic platforms

An electronic platform is an electronic interface that allows direct online contacts between several people in order to provide a supply or service. Anyone who enables delivery with the help of an electronic platform by bringing seller and buyer together to conclude a contract is considered a service provider vis-à-vis the buyer. In this case, there is a supply between the Electronic Platform and the Seller as well as between the Electronic Platform and the Buyer.

For platform taxation, only electronic platforms that enable the sale of goods are affected. Electronic platforms that make other deliveries, e.g. the rental of goods or the provision of a service are not directly affected. However, they will now also be obliged to provide information to the Federal Tax Administration about the annual domestic turnover of the various providers operating on the platform. The VAT provisions apply to both Swiss and foreign electronic platforms.

Platform operators who only take on supporting functions and are therefore not considered service providers in the tax sense are not affected by platform taxation. This includes operators who are neither involved in the ordering process nor generate sales that are directly related to the business. Also excluded are providers who only take care of payment processing, provide advertising space, provide advertising services or redirect buyers to other platforms.

How platform taxation works

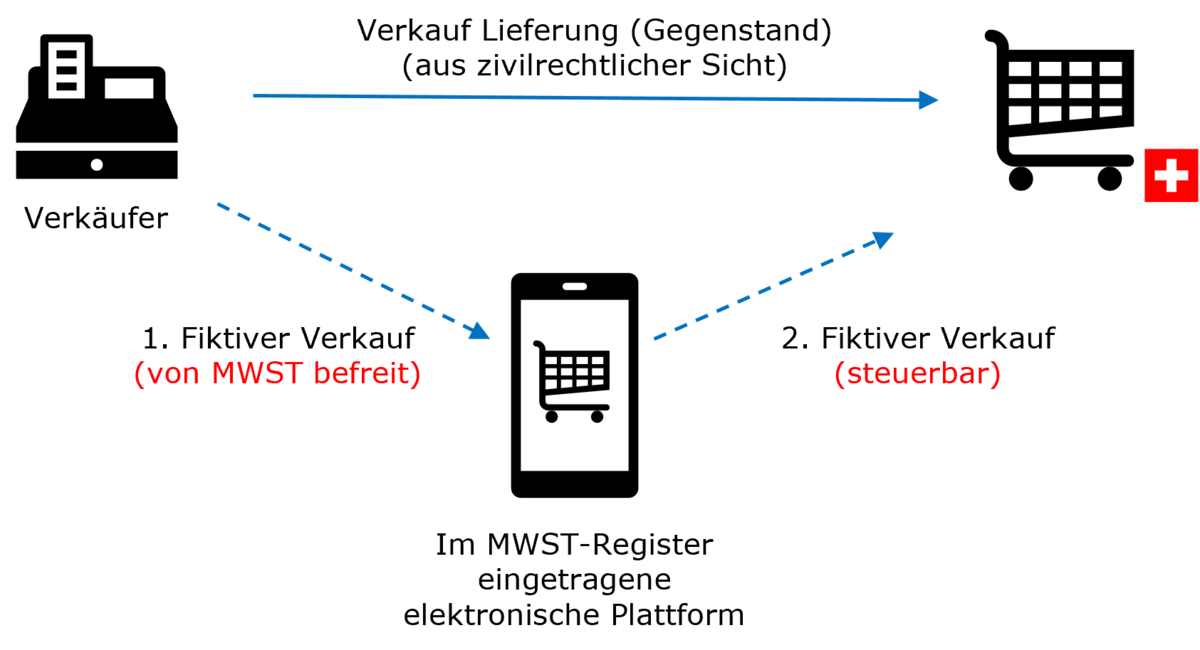

The sale of an item via an electronic platform creates two fictitious consecutive service relationships: first between the original seller and the electronic platform as the recipient of the service, and then between the electronic platform that is considered to be the new service provider and the buyer in Germany. If the platform is registered in the VAT register, the first (fictitious) supply between the seller and the platform is either treated as having been made abroad or as exempt from VAT. Foreign sellers who only provide such services are therefore not subject to VAT obligations.

From a VAT point of view, electronic platforms are treated as if they had bought the goods from the supplier and then resold them to the final consumer, even if, from a civil law point of view, the supplier is the actual seller of the goods to the final consumer. Therefore, the second (fictitious) supply from the electronic platform as the supplier of the goods to the domestic seller is taxable. The electronic platform is therefore responsible for calculating, collecting and remitting VAT to the Federal Tax Administration (FTA).

When does an electronic platform become subject to VAT?

An electronic platform is subject to VAT in Switzerland if it generates at least CHF 100,000 in turnover per year with services that are not exempt from VAT and is either established in Switzerland or provides services whose place of supply is in Switzerland. The place of supply is in Switzerland if the items are already in the country or if a foreign electronic platform generates at least CHF 100,000 in turnover with small consignments imported into Switzerland.

Consequences for electronic platforms

From 1 January 2025, shipping trading platforms will be obliged to declare and pay tax on all deliveries of goods processed via their electronic platform. To ensure compliance with these new regulations, the FTA can take administrative measures if platforms or companies wrongly fail to register or comply with their billing and payment obligations. Possible measures include an import ban on the shipments in question and, ultimately, the destruction of the goods.

Conclusion and need for action

From 1 January 2025, sales of goods made to a domestic buyer via an electronic platform subject to VAT will be directly attributed to the electronic platform. The electronic platform must therefore collect VAT on the fictitious sale of the supply to the domestic customer and pay it to the FTA.

Platform taxation is a complex issue. Potentially affected parties should therefore carefully consider which VAT obligations and possible changes will apply to them from 1 January 2025.

For an electronic platform, this includes, among other things, the correct invoicing of buyers in Switzerland, the proper processing of VAT and the declaration of taxable transactions to the FTA.

Sellers who sell their products to domestic buyers via electronic platforms will have to check whether they will continue to have to collect VAT on sales, or whether the electronic platform will now have to collect VAT on the domestic buyer, and whether the electronic platform in question will be covered by the new taxation regime. Sellers should also be aware that they are subsidiary liable for the VAT that is attributable to their platform sales and must be paid by the electronic platform. They should therefore check whether the platform through which they sell their products behaves in accordance with the rules, in particular whether it is registered in Switzerland for VAT purposes.

By Vischer, Switzerland, a Transatlantic Law International Affiliated Firm.

For further information or for any assistance please contact switzerland@transatlanticlaw.com

Disclaimer: Transatlantic Law International Limited is a UK registered limited liability company providing international business and legal solutions through its own resources and the expertise of over 105 affiliated independent law firms in over 95 countries worldwide. This article is for background information only and provided in the context of the applicable law when published and does not constitute legal advice and cannot be relied on as such for any matter. Legal advice may be provided subject to the retention of Transatlantic Law International Limited’s services and its governing terms and conditions of service. Transatlantic Law International Limited, based at 84 Brook Street, London W1K 5EH, United Kingdom, is registered with Companies House, Reg Nr. 361484, with its registered address at 83 Cambridge Street, London SW1V 4PS, United Kingdom.